Last updated on October 9th, 2023 at 01:02 pm

NEFT, RTGS and IMPS are the three conventional mode of payment option available for fund transfer between different bank accounts.

If you are a user of the Online Banking services like Internet Banking and Mobile Banking, you might have come across these terms.

Each type of transaction comes with different personalities and used for different reasons. If you do not know what type of transfer you need to do, Do not worry as this post will help you choose a right option for you.

Let see what how each type of transaction works.

What is NEFT (National Electronic Fund Transfer)?

National Electronic Fund Transfer (NEFT) is an economical option for transfer of funds between bank accounts.

NEFT is a electronic fund transfer system created by Reserve Bank of India (RBI) with an aim to create simple and accessible fund transfer facility between banks.

NEFT setup is established and managed by Institute of Development and Research in Banking Technology (IDRBT).

In NEFT transfer Transactions are done in a batches. NEFT is done in 48 Half Hourly batches. Thus resulting in 48 batches in a day.

This facility is available 24*7*365 for the users. The NEFT transfer can be done through both Official Mobile Banking and Internet banking of the NEFT enabled banks. You can also give request of transfer through bank branches with the application.

RBI also instructed banks to not charge any fee for the NEFT transaction done through online. However the banks can charge for the transaction initiated from branch at their discretion.

Also there is no upper limitation in Transaction amount. The minimum transaction for NEFT is Rs. 1 and there is no maximum limit.

What is RTGS (Real Time Gross Settlement)?

Real Time Gross Settlement (RTGS) is as opposed to NEFT is a gross settlement Payment System.

RTGS is introduced for doing the business transaction of higher value and make a quick settlement between accounts in different banks.

In RTGS transfer of fund happens in real time basis. Thus there is no waiting period or batch settlement as in the case of NEFT.

RTGS transaction facility is available 24*7 all year long even on the bank holidays. You can do the transaction through Mobile Banking, Internet Banking and through Bank Branch counter.

RTGS does bear charges for transaction from bank, which varies with the bank policy. You can check the charges from the official website of your branch on the Service Charges disclosure page.

In RTGS there is a limit for minimum transaction amount. RTGS can be done for the transaction value of Rs. 2 Lakh and above.

What is IMPS (Immediate Payment Service)?

Immediate Payment Service is a real time payment system for the lower amount transaction.

IMPS is available through Banks Internet Banking and Mobile Banking portals.

IMPS usually bears more charges than NEFT. But the amount is settled in a real time basis.

IMPS transaction can be done with the Account Number and IFSC code of an account. Also you can do transaction with the MMID (Mobile Money Identifier), MMID is an unique ID provided to each account by your bank.

Unified Payment Interface (UPI) also is build on the model base of the IMPS.

IMPS is available for customers 24*7 even on bank holidays. IMPS service generally not available through bank branch (Confirm the same by contacting your branch).

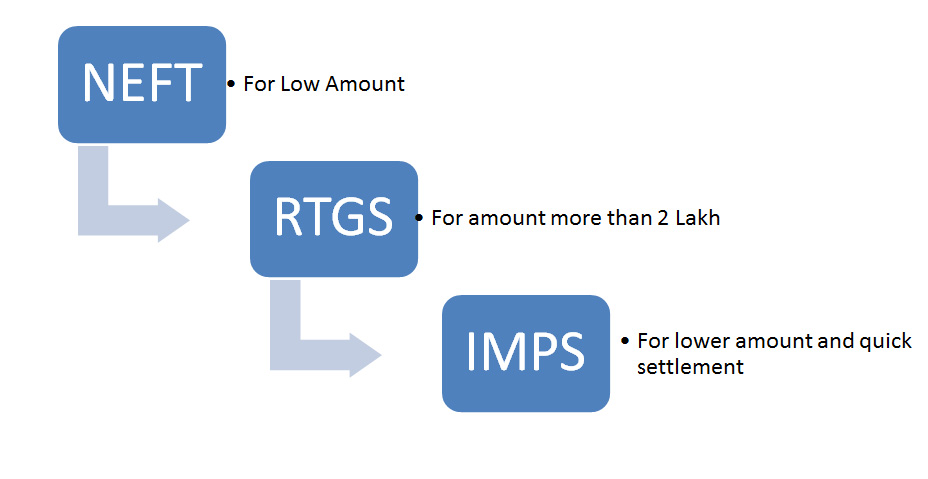

Comparision: NEFT vs RTGS vs IMPS

Thus to summarize the features of the all settlement systems. We will compare some of the basic factors.

Thus take a closer look on all the criteria as per your interest and requirement and choose best option for your need.

| NEFT | RTGS | IMPS |

| National Electronic Fund Transfer | Real Time Gross Settlement | Immediate Payment Service |

| Minimum Transaction amount is Rs.1 and There is no Maximum transaction limit | The Minimum Transaction limis is Rs. 2 Lakh and there is no Maximum Limit | There is no Minimum and Maximum Limit |

| Settled in Half Hourly Batches. | Settled in Real Time | Settled in Real Time |

| Available through Mobile Banking, Internet Banking and Bank Branch | Available through Mobile Banking, Internet Banking and Bank Branch | Available through Mobile Banking and Internet Banking |

| There is no charges for the transaction done on digital mode. There is a charges for the transaction through Bank Branch | Charges are applicable as per the Banks discretion | Charges are applicable on all mode. Usually higher than the NEFT and RTGS |

| Used for Transaction of Low amount | Used for the higher transaction amount | Used for Low Transaction Amount for faster settlement. |

Conclusion

Thus from the comparison of all the settlement system you can opt for the best option. The best option for you will differ for the each occasion as per requirement.

But if you are still unsure about choosing follow the following simple rule.

If you want to make a settlement urgently even by paying higher charge use IMPS for smaller amount and RTGS for Higher amount (More than 2 Lakh).

If you just want to make a transaction without time constraints it is better to do NEFT even for the larger amount. As this will reduce the charges paid for the transaction